Wine connoisseurs speak of the terroir of a wine, the specific characteristic that it acquires by virtue of where the grapes grow. With a New Year just underway, it may be well to mention that a firm conviction of the significance of terroir is the reason the French are unhappy when the makers of sparkling wines from anywhere outside of Champagne call their product “champagne.”

Wine connoisseurs speak of the terroir of a wine, the specific characteristic that it acquires by virtue of where the grapes grow. With a New Year just underway, it may be well to mention that a firm conviction of the significance of terroir is the reason the French are unhappy when the makers of sparkling wines from anywhere outside of Champagne call their product “champagne.”

This is our concern at AllAboutAlpha because Balter Capital Management has just prepared a statistical review of hedge funds on the basis of the cities in which they are located, its Hedge Fund Regional Performance Study. It is a study of the possible terroir of alternative investment management.

Brad Balter, in a recent interview, expanded on the reasons for this study. Hedge fund partners and traders in a given city socialize together, they talk shop, and they may have histories together in other local institutions before opening their hedge fund firms. They may naturally develop locally distinctive ideas and practices, such as the value emphasis in Boston, or the relatively lower fees distinctive to Dallas. It seemed appropriate, he said, to study systematically the concentration of ideas, and its impact on both performance and risk.

Preliminary Study

For the purposes of this study, which is professedly open to improvements and expansions going forward, Balter Capital started with seven different U.S. cities with significant hedge fund activity: Boston, Chicago, Dallas, Greenwich, Los Angeles, New York, and San Francisco.

The authors acknowledge that this inaugural study of the question of the significance of locale contains certain biases. These are for the most part the same biases that affect hedge fund indices: selection (some managers report results consistently and thus get on the radar for such studies, others don’t); survivorship bias; backfill bias.

But those biases would presumably affect all cities equally, so they would not necessarily prejudice the comparative purposes of this study.

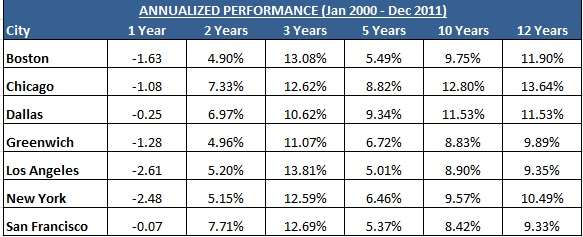

Working with a database including the period from January 2000 through December 2011, and listing cities alphabetically, relative performance is as follows:

Source: Balter Capital Management: Hedge Fund Regional Performance Study, Dec. 2012

Chicago was the best performing of the cities for the aggregate of that 12-year period, Boston second. Early in the period, and indeed until as late as 2007, Boston was either ahead of Chicago or effectively tied with it. The worst performing were: San Francisco, Los Angeles, and Greenwich. In the case of Greenwich there is a mitigating consideration, which we’ll get to below.

One thousand dollars invested with a Chicago fund would have gained, averaging both that city’s funds included in the study and the 12 years involved: 13.64 percent annually. The equivalent figure for Boston is 11.9 percent. For underperforming San Francisco, it is only 9.33 percent.

Different Correlations

Hedge funds in different cities show different portfolio characteristics. New York and San Francisco each has a high correlation to global equity markets, two cities in the middle of the continent, Dallas and Chicago, have the lowest such correlations.

Chicago also has the highest correlation with the Barclays Aggregate Index and the Barclays U.S. Treasury Index. This is intuitive: Chicago has a high concentration of commodity trading advisors. Chicago also has the highest correlation with global macro and CTA strategies as measured by the HFRI Macro and Barclays CTA indices respectively. The CTA connection, again, seems intuitive. But the degree to which Chicago tracks HFRI Macro seems a bit surprising – this correlation is closer than that between the same index and the Greenwich managers.

New York has a very high (0.88) correlation to the Russell 2500 index. The authors attribute this to active involvement by New York hedge fund managers in the trade in mid-cap securities, “perhaps to the point where they may be influencing the behavior of the underlying index.”

City Themes

The study’s authors think the distinctions among cities are not accidental, and they suggest some explanations.

There are “numerous high profile value oriented hedge funds in Boston” and its performance is generally consistent with its being a value town.

In Dallas, managers have lower compensation structures than in other parts of the U.S. Its high profile managers also had a short subprime trade on by 2007, which may account for its “much lower down market capture and beta.”

Greenwich was a below-average performer during the period under study taken as a whole. But there is an important mitigating result: it was a stand-out from the point of view of risk management, with strong risk adjusted returns that yield a Sharpe ratio of 1.32, and lower correlation with broad market indices.

Los Angeles is the site of several large credit \-focused firms, which helps explain its disappointing performance in this period and its high correlation to high yield bonds.

San Francisco is not only an underperformer but “a particularly poor performer during periods of market stress.”

One of the periods of market stress during the time frame under consideration was that of the dotcom bust, 2000 to 2002. It is to be expected that hedge funds managed out of San Francisco had extraordinary exposure to that Silicon Valley-epicentered earthquake. More generally, hedge funds in that city seem to be “managing their portfolios aggressively, with outsized exposure to technology as a whole.”

Balter itself is headquartered in Boston, a registered investment adviser focusing on hedge fund investment and research.