By Artem Milinchuk, Founder & Head of Strategy of FarmTogether.

Throughout the United States' history, a number of recessions have caused investors to reconsider their portfolio allocation transition to 'risk-off' strategies, such as U.S. treasuries and real assets.

To explore an additional option for investors, here, we look into four US recessions and how farmland has performed with key takeaways to apply to the current environment.

Investing in Turmoil

During market uncertainty or recessions investors look for these essential attributes to maintain and grow their wealth:

- Safe Havens

These assets are most often real assets with tangible value; they're perceived as risk-free or close to risk-free. The most well-known are gold, which typically spikes in price with market fears, or US short-term debt, like TBills, which even briefly had negative yields (e.g., investors would pay to hold them) in the most recent recession.

- Low Volatility

With market fluctuations creating swings that impact net worth nearly day-to-day, assets with a lesser tendency to do so, like US bonds or Gilts, provide a welcome peace-of-mind.

- Uncorrelated to Stocks

As the economy slows in a recession with GDP growth dropping to, or even below, zero, equity prices will often fall, reflecting the bleak future outlook. Investors seek uncorrelated assets that won't be impacted in the same way as stocks.

- Positive Returns

In a struggling economy, investors still seek opportunities to grow their wealth with either income-generating assets, with essentials like residential rentals, or inflation-adjusted income streams like TIPS.

Below are Four Case Studies Highlighting Recessions in US History and Demonstrating Their Impact on Farmland Values

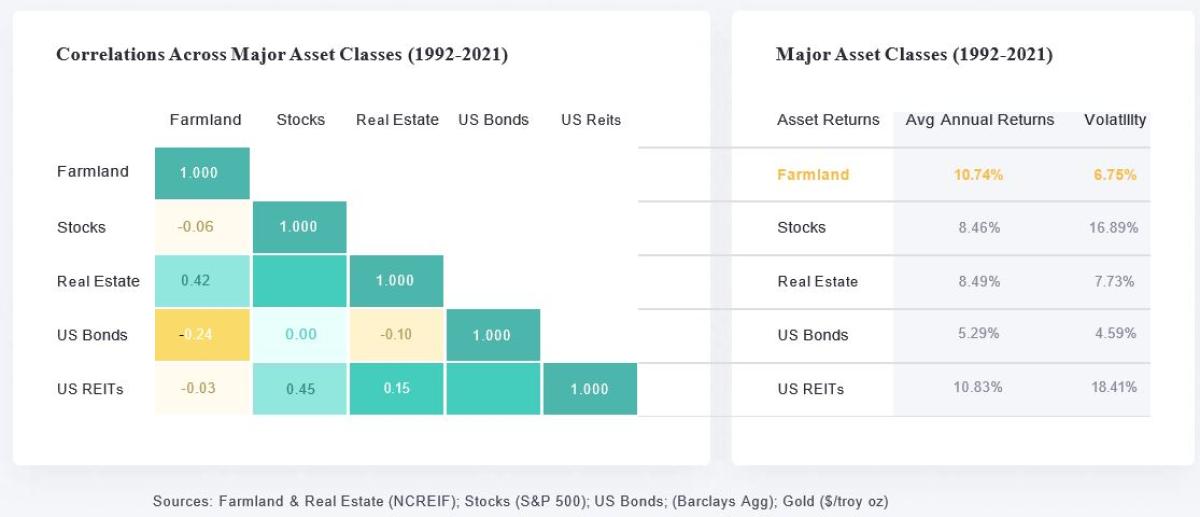

These same attributes appealing to investors through turmoil into a recession are also characteristics of farmland, making it a viable alternative/addition to traditional assets. Farmland is a tangible asset with intrinsic value, like gold, with returns uncorrelated to stocks, and with volatility closer to bonds. It's a "goldilocks-zone" asset. As an investor, it's essential to consider the factors driving farmland values as well as anticipated risk-adjusted returns for alternative assets at any point in time.

Farmland values are dictated by global factors (e.g., population, climate, long-term commodity prices, pandemics), national factors (e.g., interest rates), and all the way down to parcel-specific attributes like soil quality and water rights. A few overarching trends worth noting through the last half of the century and going forward are population growth, which will continue as the UN anticipates reaching nearly 10 billion by 2050, as well as a steady decline in farmland acreage. In the United States, total farm acreage has been on a steady decline. decreasing by nearly 20% since the mid-1960s according to the USDA. In 2012 - 2017 alone US lost 14 million acres, roughly the size of West Virginia.

To elucidate how various considerations come together to influence farmland values, we've prepared four case studies highlighting recessions in US history and their impact. We'll discuss the Great Financial Crisis in the late 00s, the Dotcom Bubble at the turn of the century, the 1980s Recession, and the COVID-19 pandemic in 2020.

Case Study #1: Financial Crisis

Subprime mortgages and derivatives were used widely throughout the financial system. As housing prices begin to fall in 2006, it set off a chain of events that left the economy in shambles. Unemployment hit 10% in 2009 and the Federal government had to bail out many major financial institutions with TARP. Some notable institutions (e.g. Bear Stearns, AIG) went under, and the Federal Reserve was desperately trying to inject liquidity with quantitative easing and rate cuts.

Alternative Investments

The fall 2008 sell-off in the equity markets eventually led to nearly $8 trillion dollars of losses for Americans by the end of the Financial Crisis. Typically, fear would lead investors to move toward real assets like real estate and gold or other safe-haven assets like US bonds. In a crisis that started with a housing bubble, where American losses in home equity alone are estimated to be north of $ 3 trillion in under two years, conventional real estate returns provided no comfort to investors.

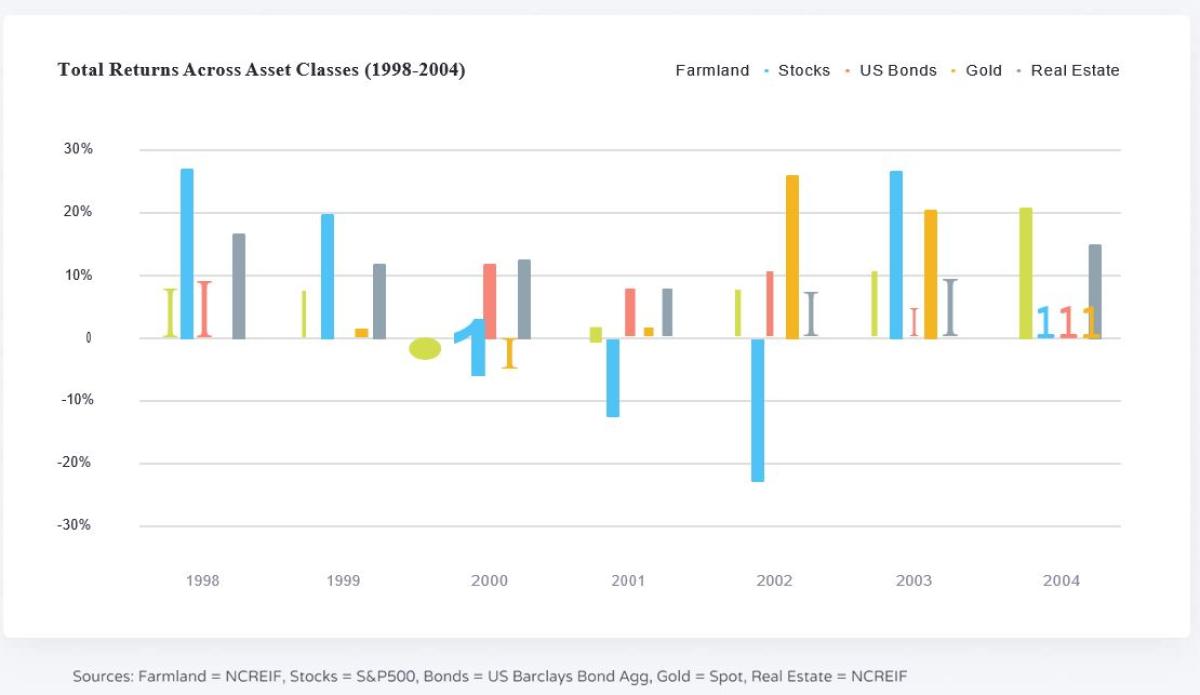

The flight to safety led investors toward gold and US bonds, even briefly turning TBill yields negative as investors were willing to pay for security. Those assets, as well as farmland, produced consistently positive returns throughout the period. From the first quarter of 2007 to the fourth quarter of 2009, farmland returns were up nearly 30% and gold over 60% while equity and real estate both fell by double-digits.

Farmland Value Drivers

While the Federal Reserve tried to mediate the economy with low interest rates, farmers' balance sheets and thus farmland values benefited from lower debt payments. Low rates also enabled predominantly credit purchases in 2008 and 2009 for farmers. Farm income was aided by higher commodity prices, which again, contributed to sustained farmland values. The tumultuous environment in the rest of the country meant continued returns and continued flight to safe assets.

Idiosyncratic factors in local farmland markets, particularly related to housing market losses, did cause some areas to lose marginal value for a couple years, especially in the Northeast. Specifically, farmland near urban centers, with more expensive residential and commercial real estate, can have its value partially impacted by proximity. A dramatic fall in the traditional real estate market had some knock-on effects in farm real estate.

The Period Highlights Several Key Points:

- Farmland is Not Like Other Real Estate

The real estate bubble that ultimately led to the financial crisis and a crash in conventional real estate values, did not create a one-to-one transfer in farmland values. The slight influences were only in specific geographies more prone to development.

- Low Rates Are Good for Farms

Low rates help support farm balance sheets, especially with manageable debt-to-asset ratios, as it's easier to maintain debt payments for mortgages and other large purchases. Rates in the current environment are the same as 2008-2009 levels.

- Farmland vs. Equities

Negative returns and high volatility in equities don't translate to the same with farmland returns as the two are generally uncorrelated.

Case Study #2: Dotcom Bubble & 9/11

The early 2000s were marked by the boom and bust of tech with Pets.com famously going bankrupt only 9 months after its IPO. The following September in 2001, fear and uncertainty from the tragic terrorist attacks on the World Trade Center caused further declines. By mid-2003 the Fed rate was the lowest (0.75%-1.0%) it had ever been to date as the Federal Reserve attempted to combat lingering unemployment.

Alternative Investments

Investors in the S&P 500 over the first three years of the century would have lost over 40% as stocks tanked, more if their equity holdings were disproportionately technology stocks which fell even further. The ultimately unmerited Y2K fears caused a spike in gold in 1999 as people flocked to the tangible asset followed by a reversion later. US Bonds provided consistent and safe returns throughout the period. Real estate would have appeared consistent and alluring as the early 2000s housing bubble was leading into the Financial Crisis.

Farmland Value Drivers

Farmland values benefited, in part, from the rising real estate market across the country. Land prices in fact grew as fast, if not faster, than real estate in many rural states according to the USDA's reporting. Increased demand for ethanol beginning in 2002 contributed to corn demand and thus land prices. Similar to the Financial Crisis, low interest rates aided the farm economy with cheaper borrowing and cheaper debt repayments.

This Period Highlighted a Few Key Points:

Farmland Value Drivers

Farmland values benefited, in part, from the rising real estate market across the country. Land prices in fact grew as fast, if not faster, than real estate in many rural states according to the USDA's reporting. Increased demand for ethanol beginning in 2002 contributed to corn demand and thus land prices. Similar to the Financial Crisis, low interest rates aided the farm economy with cheaper borrowing and cheaper debt repayments.

This Period Highlighted a Few Key Points:

- Farmland vs. Gold

Farmland is a tangible asset with an intrinsic value that can provide a safe haven for investors, similar to gold. However, it is typically much less volatile. Also, unlike gold, farmland has utility and provides annual income via the sale of its harvest.

Agricultural Products Are Essential

Farmland produces food, fiber, and fuel - all essential to our life.

- Farmland is Low Volatility

Farmland returns are more stable than either equities or gold, which are prone to fear- and uncertainty-driven volatility.

Case Study #3 - 1980s Recession and Inflation

Trying to combat a 10% inflation rate following the US unpegging its currency from gold, the Federal Reserve Rate reached a record high of 20% in 1979 and 1980. Coupled with an OPEC-induced energy crisis, the US was hit with a recession in 1981. As a result, unemployment peaked in 1982 & 1983 at 10%. High interest rates remained throughout the first half of the decade.

Alternative Investments

Throughout the period, investors lacked any standout quality investment options. Bonds appeared most attractive with consistent returns but adjusting for inflation in the late 70s they didn't actually produce positive returns. Stocks were a close second, though had negative returns in 1981. Gold hit

$850/oz on January 2nd, 1980, with growing inflation and uncertainty, though fell back toward 1978 levels by the middle of the decade with negative returns in 1981. Gold's volatility stood out compared to alternative assets. Real estate returns were relatively moderate and consistent.

Farmland Value Drivers

Strong grain prices in the late 1970s made it easy and appealing for farmers to borrow, expanding their operations. In the following years, between surplus grain production, a strong dollar, and President Jimmy Carter's Soviet Grain Embargo in 1980, agricultural exports fell by nearly 20% from 1981 to 1983. Grain prices plummeted. Simultaneously, farmers faced rising production costs, like increasing oil prices. The Midwest states, which grow the most corn, soybeans and wheat, were most affected.

The Federal Reserve's high interest rates in an attempt to quell inflation combined with decreased farm incomes, caused farmland values to fall. The average price per acre for US farmland fell by just over 4% in 1983, the first decline since the Great Depression. Lower farmland values, then the primary asset used to secure farmland debt, in turn, made farm debt increasingly hard to service.

Best estimates1have farm bankruptcy rates higher than the Great Depression as a result, which only further depressed farmland values. The continued downward spiral led to the only two years of (only slightly) negative farmland returns post World War 112• This shows the resilience of farmland even in the most adverse conditions.

The Period Highlights a Few Key Points:

- Be Wary of Too Much Debt

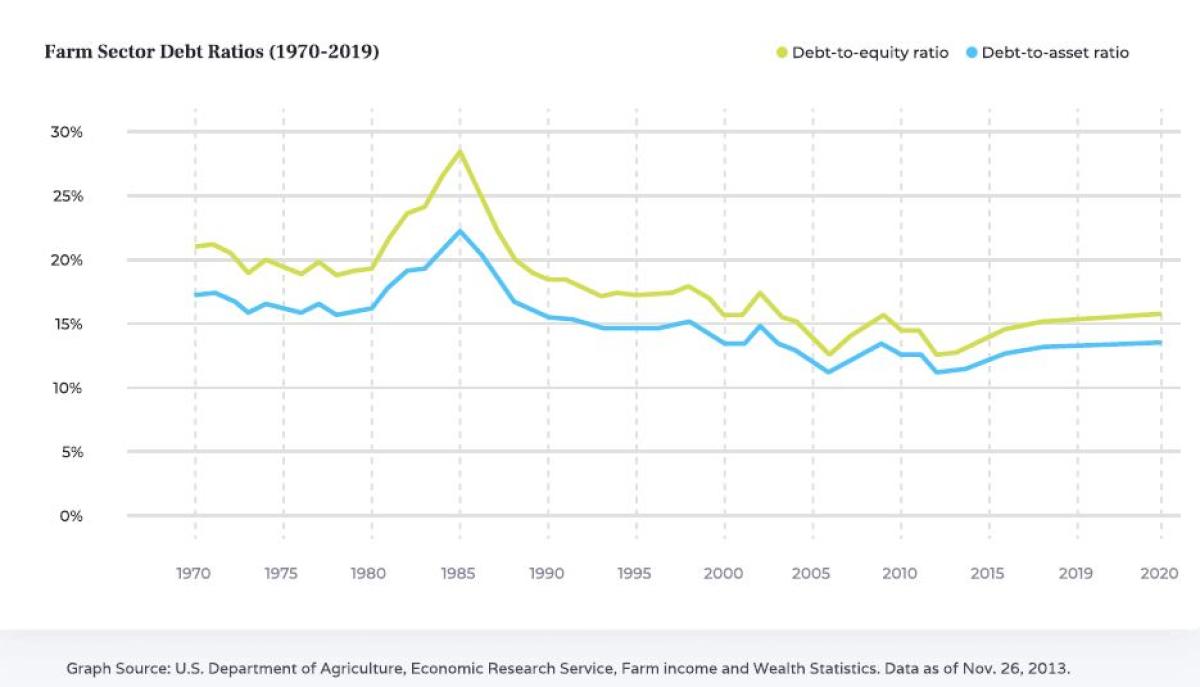

The farm sector was too highly levered. Farmland productivity growth in the 1970s made lenders eager and they used rising farmland values as collateral for loans in lieu of a cash-flow analysis3• This is not the case today: loans are based on revenue estimates and modern crop insurance provides revenue coverage not available then. Now, debt-to-asset ratios are below 15%, far below the 22% of 1985.

- 1980s' Interest Rates Are Not Today's

In the only two years where farmland returns have been negative in almost a century, the country had nearly double-digit interest rates and inflation. Year-to-date, we are experiencing a similar reality with respect to inflation, as the year-over-year inflation reached 8.3% - near the 40-year high of March 2022 of 8.5%.

Despite the highest inflation in 40 years, interest rates remain well below their highs of the 1980s. The onset of the Covid-19 pandemic in March 2020 led to the Federal Reserve's extremely accommodative monetary policy to dampen the impact of worldwide shutdowns. Now, with inflation ramping up over the past several months, the Federal Reserve is moving to a hawkish position. At the May meeting, the Fed announced a 0.50% increase to their benchmark to a new target range of 0.75% to 1.0% and has signaled for further increases this calendar year.

- Institutional-Quality Management of Permanent Crops

Our sourcing & underwriting process and farm management provides clients with access to institutional-quality investments and oversight. For this final case study, we used TIAA-CREF estimates for farmland returns as a proxy, however, this data does not reflect institutionally managed properties like the NCREIF Farmland lndex3used in prior cases. The NCREIF Index representing institutionally managed farmland provides higher average returns for its lifetime as compared to the TIAA-CREF estimates.

Case Study #4 - Covid-19 Pandemic

The Covid-19 pandemic began in January 2020, when a mysterious flu-like illness struck several people in Wuhan, China. By mid-March, the World Health Organization had declared Covid-19 a global pandemic. Countries around the world issued stringent travel restrictions and widespread business closures to stem the spread of the disease.

These shutdowns and the ensuing panic around the potential repercussions of the unknown disease led to a rapid collapse of the stock market. In lieu of stocks, investors moved large amounts of capital into highly liquid safe haven assets.

Alternative Investments

The market disruptions led to significant government stimulus, Fed rate cuts, and renewed quantitative easing, which drove historically low bond yields. In March 2020, Gold prices dropped by 4 percent, while bitcoin's value dropped by 50 percent in a single day. Bitcoin prices have since rebounded, but volatility persists. Commercial real estate produced anemic returns as most segments, including hotels, office buildings, and brick-and-mortar retailers were operating at drastically reduced capacity or completely shut. The long-term impact of Covid on commercial real estate remains to be seen.

Farmland returns in 2020 were the lowest since 2001 due to a confluence of factors, including the trade war with China, disruptions in the supply chain, low commodity prices, labor shortages, and reduced demand for biofuels. These returns were almost entirely attributable to income rather than price appreciation.

Farmland Value Drivers

US farmland provided a total return of 3.1%, nearly 7.5 percentage points below the 10-year average. This uncharacteristic performance was not evenly distributed across crops or regions. Annuals crops performed better than permanent crops, providing total returns of 4.2%, as the negative impact of reduced biofuel demand was partially offset by an increase in demand for feedstock. Permanent crops provided total returns of only 1.3%, including negative appreciation. This was heavily influenced by the poor performance of almonds and wine grapes, which make up a large portion of the NCREIF Farmland Index.

Similarly, total US farmland returns were significantly impacted by poor performance in the Pacific Northwest, Pacific West, and Mountain regions, which together accounted for ~56.1% of the NCREIF by value. All regions experienced positive cash income, albeit reduced, and negative appreciation, in part due to the underperformance of their major crops. Although 2020 was an underwhelming year for US farmland, it held its returns much better than the stock market, as was the case in prior recessions. Over the last 50 years, the value of American farmland has risen by about 6% per year, with only five down years during that period.

The Period Highlights a Few Key Points:

- Farmland Is Not A Homogenous Sector

The impact of the Covid pandemic varied widely by region and crop type. Certain crops and regions were also impacted by unique, idiosyncratic factors in addition to wider macroeconomic trends related to the pandemic.

- Farmland Provides Positive Current Income Even If Appreciation Is Low

Every region in the US produced positive income in 2020, which mitigated the impact of lower appreciation.

- Farmland Is A Safe Haven Investment

The relative stability of farmland throughout the Covid pandemic illustrates its value as a safe haven investment. Farmland is a low-volatility asset class that acts as a store of value in turbulent economic times. Compared to gold, another safe haven investment, farmland offers the additional benefit of passive income.

Conclusion

Farmland has low volatility, reliable capital appreciation, and an income stream from harvesting crops. It has proven to be a stable asset historically, providing diversification to a traditional portfolio with its uncorrelated returns. Diversification is critical for reducing portfolio volatility and building wealth over the long term. Investors are increasingly turning to alternative investments to provide this diversification, including collectibles, commodities, cryptocurrency, real estate, or farmland, especially during threats of a recession. Demand for farmland specifically among institutional investors continues to explode. In 2005, there were less than 20 farmland-focused investment funds globally. This began to change following the 2008-2009 financial crisis, as more money began flocking to safe-haven investments like farmland. By 2020, the number of funds specifically focused on farmland had ballooned to 166. With fears of inflation on the horizon, we ant1c1pate with the farmland returns, which move in lockstep with CPI, to continue on a stable, positive trajectory going forward.

Footnotes:

I. Changes to US bankruptcy regulations mean farm bankruptcy data is unavailable from 1978-1986

2. Source: TIAA-CREF Center for Farmland Research calculated data.

3. TIAA-CREF estimates by & large track the NCREIF Farmland Index (over 60% correlated from 1991-2018), however the NCREIF, representing institutionally managed farmland, has outperformed consistently for the past 15 years and has higher average annual returns (11.2% vs. 8.5%) since inception.

4. Sources: USDA, Hancock Agriculture Q4 2020 Farmland Investor, Callan Pandemic, Valoral Advisors Food and Agriculture.

About The Author:

Artem Milinchuk, Founder & CEO of FarmTogether. Artem has over 10 years of finance experience in food, agriculture, and farmland.

Prior to founding FarmTogether, Artem was employee #1 and CFO/VP of Operations at Full Harvest Technologies, a now post-Series A B2B platform for buying and selling produce. He previously worked at Ontario Teachers' Pension Plan, Sprott Resource Holdings, E&Y and PwC. Artem holds an MBA from The Wharton School, and a BA and MA in Economics from the Higher School of Economics.