The boards of directors of mutual funds serve a valuable role when those mutual funds have securities-lending operations. The directors are monitors, and from the filings that registered investment firms make to the Securities and Exchange Commission it is possible to make some broad inferences about the type of board and board member who is associated with higher returns on such an operation.

The boards of directors of mutual funds serve a valuable role when those mutual funds have securities-lending operations. The directors are monitors, and from the filings that registered investment firms make to the Securities and Exchange Commission it is possible to make some broad inferences about the type of board and board member who is associated with higher returns on such an operation.

That is the takeaway from a newly published paper by John C. Adams of the University of Texas at Arlington, Sattar A. Mansi of Virginia Tech, and Takeshi Nishikawa of the University of Colorado at Denver.

Independent, Busy, and Non-Excessively Paid Directors

The paper, Affiliated Agents, Boards of Directors, and Mutual Fund Securities Lending Returns concludes that lending returns rise as boards become more independent. For purpose of this correlation, what matters is the number of independent directors, not the independence of the chair specifically. A related finding: it’s a good sign for lending returns if the independent board members are members of other boards. This may simply mean that the more in-demand directors are the better monitors, so they get invited to serve at more than one place.

Separately, it is a good sign if the directors have, as the saying goes, “skin in the game.” Annual securities lending returns “are, on average, about 1 [percent] higher when directors own shares in the firms they monitor.”

Perhaps most fascinating, the effectiveness of directors as monitors especially in the securities lending context may be inversely correlated with their pay, beyond a certain non-excess level. The most highly compensated directors “may fear losing their positions and therefore may not adequately monitor” the lending program at issue.

The authors of this paper observe that there is a relationship between their research and that of Richard Evans et al., who recently found that lending funds underperform non-lending funds. Evans et al. attribute this to restrictions on the ability of mutual funds to sell certain stocks. They can hedge their exposure to downdrafts by lending out securities that they aren’t able to sell.

The Database

Adams et al are specifically interested in index funds, in part because the passive nature of such funds bars them from any active decision to sell securities (and reduces the recall risk to those who borrow securities from them).

Registered fund managers file annual and semiannual certified shareholder reports (N-CSR and N-CSRS respectively) with the Securities and Exchange Commission, and the securities lending data in these filings made up a good part of the database for the study. Wherever such lending forms 5 percent or more of the funds’ gross income, it must be broken down as such in these reports. Below that threshold, such income can be lumped into the “other income” category.

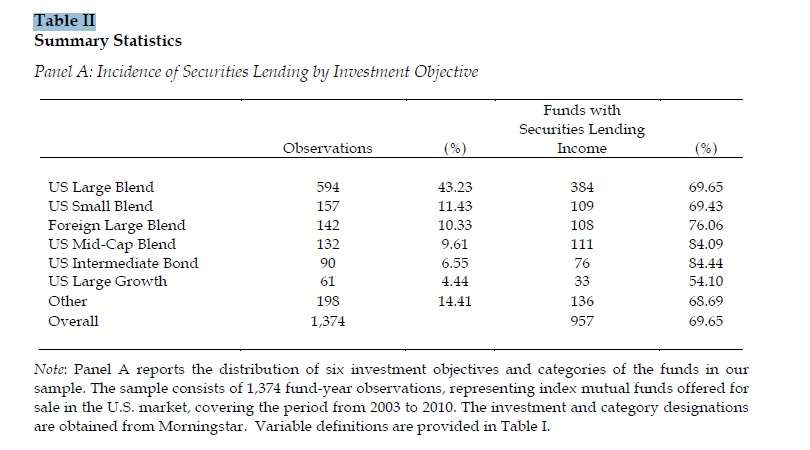

As the above Table indicates, the authors compiled a database consisting of 1,374 fund-year observations, with a range of fund categories and investment objectives represented. In one of those categories [U.S. intermediate bond], the incidence of securities lending at or beyond the 5 percent reporting threshold mentioned above was 84.44 percent. That same category has close to 11 percent of its portfolio securities on loan.

Affiliated Agents

Aside from the role of the directors, the authors concerned themselves, as the title of their study indicates, with the question whether a conflict of interests exits – and whether it has a bottom line cost – when mutual funds hire securities lending agents that are affiliated with their sponsor. The answers are “yes, and yes.” Sponsor-affiliated lending agents correlate with lower annual return on the lent securities.

Income from the securities-lending business is itself of two sorts. There are the direct lending yields and there are the profits of the re-investment of the borrowers’ collateral. But taking them both into account, “when funds administer their own lending programs and collateral reinvestments their securities lending returns are higher than the returns of funds that employ agent lenders, especially during periods of increased lending uncertainty. “