By Diane Harrison

It is 2013: a new year, an opportunity to start a fresh YTD performance chart, and a chance to climb a little further out of the 2012 hole in which a fair amount of the alternative investment world wallowed. January is often a time when investors and managers forge resolutions to do better — take stock of portfolios, review what seems to be working and what seems to be off, and implement a course of action for the coming year.

Fiscal cliff avoidance aside, the alternative landscape appears littered with potential pitfalls, pratfalls, and protracted performance slumps. Some of us might feel that a trip to the Galapagos Islands would be more enjoyable than diving into the fiscal waters of 2013, so it could be interesting to filter this viewpoint with a little evolutionary context courtesy of Charles Darwin.

There are many proponents and opponents of Darwin’s theory, engaging in a lively debate that has spanned more than a century. The theory goes something like this:

Darwin's general theory presumes the development of life from non-life and stresses a purely naturalistic (undirected) "descent with modification." That is, complex creatures evolve from more simplistic ancestors naturally over time. In a nutshell, as random genetic mutations occur within an organism's genetic code, the beneficial mutations are preserved because they aid survival—a process known as "natural selection." Natural selection acts to preserve and accumulate minor advantageous genetic mutations. Over time, beneficial mutations pass on to the next generation and the result is an entirely different organism (not just a variation of the original, but an entirely different creature).

(Source: www.darwins-theory-of-evolution.com)

Certain elements of the theory seem more likely to be true than false, particularly as applied to financial elements. Let’s examine five of these.

Time is a good thing. So, if one assumes that complex creatures evolve from more simplistic ancestors naturally over time, being an investor who has been around longer could mean having gained an ability to judge what is singular and what is systemic in the markets — in other words, an ability to separate the melodies from market noise. Investment managers with longevity have learned a thing or two about getting it right. Investors who have been in the market longer have also presumably learned both from their mistakes and have gotten better at identifying good choices. Ageism in alternatives means having been at it long enough to know what “it” is.

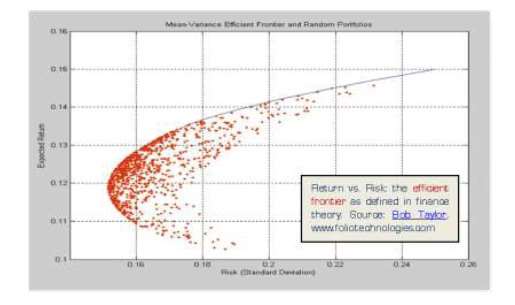

It pays not to follow the herd. According to Darwin, beneficial mutations are preserved because they aid survival. For investment managers, it literally pays to be a standout. Beneficial mutations in the investment world are the leaders, the outliers in the north-by-northeast quadrant of the efficient frontier. If they are considered beneficial, it is because they achieve performance results without taking on excessive risk in so doing. Managers who care about attracting investors are always seeking to improve their relationship with the top left quartile of the risk/reward chart. Those possessing the ability to land there and stay there are the ones who, by being better, dare the rest to follow.

Natural selection rewards the organism with a higher rate of survival. The theory goes on to postulate that natural selection acts to preserve and accumulate minor advantageous genetic mutations. If we consider the investor to be the organism, aligning interests with the talent that occupies the “beneficial mutation categories” of alternative investing leads to an elevated form of life, or perhaps a fully funded investment mandate. Less desirable species (or investments) ultimately cease to exist in favor of more desirable ones. This part of the evolution process is often in a push/pull relationship when applied to investment management. As a good alternative idea/manager/investment vehicle attracts greater numbers of followers, the ability to continue to perform at the same or higher levels of performance erodes, and other opportunities arise to take its place. One could blame greediness or complacency on the manager who fails to stave off this competition, but perhaps it’s the natural selection process in action.

Being a little bit right a lot of the time sure beats being wrong one or two mega-times. This piece of natural selection is perhaps the most recognized commonality in the alternative investing world. In the long run, if an investment manager fails to control the downside, there isn’t much of an ability to last long enough to capture the upside. For investors, swinging for the fences when making investment decisions is likely to result in knocking oneself right out of the game before having amassed enough of an investment cushion to be able to take on high-risk investments. The “stay rich” mentality of slow and steady progression through all market cycles and strong risk management practices to protect against the unforeseen happenings is the investment version of natural selection that very few alternative managers or investors care to argue against.

You can’t forecast a change, but change is a constant. While Warren Buffett may have been able to get away with the now-quaint “buy-and-hold” strategy, the markets have proven that the “buy-it-and-forget-about-it” ship has sailed and isn’t coming back. Most people would also agree that market timers, both on the buy and the sell side, are doomed to eventual failure.

While the natural selection argument is likely to continue indefinitely on into the future, with heated defenders both for and against Darwin, there is no argument about the inevitability of change. Complacency is the enemy of Darwinists, and should be of investors. Being too comfortable in deciding on a singular course of action will, over time, lead to an erosion of effectiveness in investment planning. Long-term survival in both the physical and the investment world requires vigilance, constant learning, and adaptation. As 2013 unfolds, the markets will provide undeniable opportunities and risks for both managers and investors. Those with the adaptive skills to survive will emerge fitter, smarter, and financially resilient.

Diane Harrison is principal and owner of Panegyric Marketing, a strategic marketing communications firm founded in 2002 and specializing in a wide range of writing services within the alternative assets sector. She has over 20 years’ of expertise in hedge fund marketing, investor relations, sales collateral, and a variety of thought leadership deliverables. A published author and speaker, Ms. Harrison’s work has appeared in many industry publications, both in print and online.

Contact: dharrison@panegyricmarketing.com or visit www.panegyricmarketing.com.